This articles offers a guide to nonprofit loans and how to apply for them.

A nonprofit business is any kind of organization that is exempt from paying taxes to the IRS because the business is providing a public benefit and furthering a social cause.

The donations that are made to nonprofit organizations by the public are usually tax-deductible for anyone who makes them, which can be beneficial for individuals who want to reduce the amount of tax they owe. The nonprofit business doesn't pay any tax on the donations they receive or the money that they earn from fundraisers.

The main issue with running a nonprofit business is that nonprofits still require money in order to succeed and survive. Your nonprofit won't last long if you can't pay your employees, purchase necessary equipment, and buy the right amount of office space. The eventual success of a nonprofit startup depends on how well they execute their business plan. To make sure that your business plan is implemented correctly, you will need funds. Nonprofits can make money by selling merchandise that has been donated or by performing activities that are related to their organization.

The following article offers a detailed guide on nonprofit loans, which includes information on what these loans are and how to apply for them.

A nonprofit business loan is a type of loan that's designed specifically to go to nonprofit organizations that require a certain amount of funding.

Whether you require financing for operating capital or the purchase of inventory, a nonprofit business loan can provide you with the funding that you need to reach success and to fully realize your goals as a nonprofit. In most cases, these loans are going to be below $50,000 and must be used entirely for business purposes. While this type of loan is technically available to all nonprofit businesses, it's very difficult to qualify for a nonprofit business loan, which is why it's highly recommended that you take the time to prepare for the application process.

Only a small number of lenders will provide nonprofit organizations with business loans, which makes them very difficult to obtain. The main reason that very few lending institutions provide these loans is that lending money to a nonprofit organization is considered to be even riskier than lending to a traditional business. The lender will also be required to verify that your company would classify as a nonprofit business, which means that they will take a look at everything from your fundraising plans to your total revenues.

The majority of nonprofit loans are currently provided through large donations and government grants. Because of the uncertainty of long-term success for a nonprofit organization, these loans will usually come with higher interest rates as well as a greater chance of being rejected for the loan. To heighten the possibility of being approved for one of these loans, it's highly recommended that you gather all of the necessary documentation before you begin your application.

You can make it more likely that lenders will provide a loan to your nonprofit by showing documentation that essentially guarantees you will be able to pay back the money throughout the duration of the loan. Some lenders also find it important that the nonprofits that they provide loans to have a positive reputation in the community. If you have a great reputation in your surrounding community because of the work that you've done as a nonprofit, this can increase the likelihood that your loan application is approved.

The application process differs from lender to lender. However, each lender will have some basic requirements that you must fulfill if you want your application to be approved. First of all, you will need to provide them with detailed and precise financial information that outlines all of your assets, revenues, and spending. These financial documents should go back at least two years. If you have recently formed a nonprofit startup, provide all of the financial information since your business was formed. This information will also show the lender that your business is a nonprofit, which must be proven if you want your application to be approved.

The Small Business Administration provides nonprofit organizations with a significant amount of resources on how to apply for a loan. They also offer several loans that you might qualify for. The main benefit of seeking a nonprofit loan through the Small Business Administration is that they usually offer competitive terms. When you're searching for the right lender, your criteria should be that the lender has experience providing loans to nonprofit organizations. These lenders should better understand the importance of obtaining a loan as a nonprofit, which makes it more likely that they will approve your application.

Most lenders provide borrowers with the opportunity to apply online. Once you've found a lender that offers fair loan terms, your first step should be to look on their website for an online application. If you've already gathered all of the pertinent financial information related to your nonprofit business, you should be able to complete the application in less than 30 minutes. The time that it takes for a loan application to be processed differs with each lender and depends on when the lender receives the appropriate financial documentation. If you forget to provide the lender with some of your financials, the approval process could be delayed. In general, it takes around 2-4 weeks for a nonprofit loan to be closed once the lender has received all of the documentation that they need.

Before you apply for one of these loans, it's important that you do your due diligence. Make sure that you compare the loan terms for all of the lenders that you're considering applying to. If the lowest interest rate that you can find is higher than you would like it to be, consider asking for less or waiting until your financials have steadied. If you have all of the necessary documentation at the time of applying for the loan, the application process should be fairly straightforward.

When you're considering applying for a nonprofit loan, the most important aspects of the loan are the terms, the interest rate, and the repayment plan.

The standard loan terms for a nonprofit business loan extend from 1-10 years. While you might find it advantageous to obtain a 10-year loan that you would have a long time to repay, it's important to remember that longer terms come with higher interest rates.

While your monthly payments will still be lower than they would be with a three-year loan, you would end up paying more over the duration of the loan. You should only obtain a loan that comes with a term of 1-2 years if the amount is small or if you're certain you will be able to make the high monthly payments.

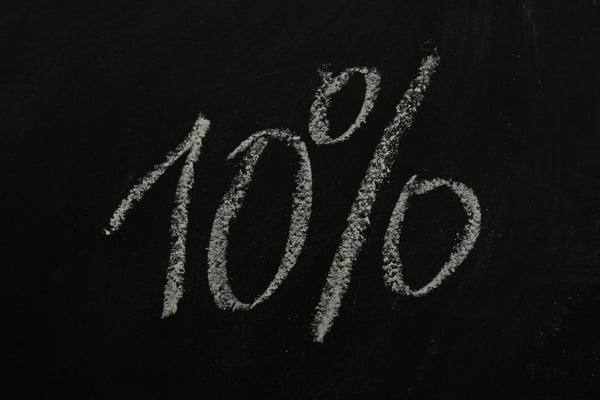

The interest rates for a nonprofit business loan usually range from 7-10 percent. You can expect to receive an interest rate in the upper end of this range if you don't have a lengthy business history of if your credit is relatively low.

While interest rates usually top out at 10 percent, there's always a possibility that a lender could allot interest rates that are as high as 20-30 percent. These loans are almost never worth it and should be avoided. With most nonprofit loans, the interest rate that you receive at the beginning of the loan will be the same that you pay at the end.

While it's possible for repayment plans to differ significantly, the majority of repayment plans require the borrower to make payments on a monthly basis for the length of the loan. If your loan lasts for five years, you will be tasked with making 60 payments over that period. The amount that you pay each month will likely stay the same unless you make a higher payment in the hopes of repaying the loan early.

While you'll almost certainly be provided with a standard repayment plan, there are many additional repayment plans that are possible with a loan if the lender is flexible. For instance, graduated repayment plans start off with lower payments that increase by a small amount every two years until the loan has been paid off in full. If your lender is offering a different repayment plan than the standard one, it's important that you fully understand what the plan entails before you apply for the loan.

While nonprofit business loans can provide you with the money you need to grow your organization, there are numerous alternatives to loans that might be better for you and your company.

Another great resource that you can tap into when you're trying to grow your business is University Lab Partners, which is a wet-lab incubator that provides startups and small businesses with lab space, office space, modern technical resources, and access to many individuals and companies in the life sciences industry. No matter what kind of financing you obtain, the resources that are available through University Lab Partners can help you grow and make good use of the money you have.

Apply now to get started!

Revised 11/17/2020

Do you have a great company in the bioscience or medtech industry? Do you need wet-lab and/or fabrication space to develop and test your product?