Learn various methods on how to value your biotech startup.

One of the many important pieces of information you will need when trying to secure funding for your biotech company is a company valuation. The start up valuation is used to determine various metrics for your potential investors, and it is important that your valuation is accurate and fair. However, attempting to value a startup can be distinctively more challenging than valuing a larger company. In addition, biotech startups pose an even more unique issue on the issue of valuation. This article details how to assess your biotech startup in order to provide the most accurate valuation for investors.

🔬 Learn about: Funding Options for Biotech Startups

The worst way to value your startup is to not value it at all, thinking that someone else will do it for you. Investors are busy people, and they expect companies to have at least an idea of what they are worth, even if the number is a bit rudimentary.

In addition, you should not try to value your company based on the dollar-amount of grants you have received, or a similar number. Your company is more complex and robust than just what you received from a grant!

🔬 Read: Finding Funding for Your Biotech Startup

Earlier we mentioned that larger and older companies have it easier when it comes to valuing their companies. Let's dive into why that is so:

Public companies are usually valued by their “Market Cap”. Market Cap is calculated by multiplying their share price times the current number of shares. This can be done with a simple formula, and gives leadership an idea of how the company is currently valued, as it changes month to month.

Private, and profitable, companies are typically valued by using public comparables. To do this they find public companies of a similar size, industry, and product-range as them, and compare the public company’s valuation to their company.

Private companies and their public comparables can be measured using various ratios, like the price to earning (P/E) ratio, or their price to sales (P/S) ratio. The private company would then use their financial statements to estimate their value based on the price ratios of the public company. If you want to roughly estimate your own ratios, use these formulas:

Of course these formulas are not exactly precise, but they can give you a good estimate of what a private company’s valuation is, if you use the P/E or P/S ratio of a public comparable.

Private companies that are not yet profitable need to use projections and comparables as compared to using their current financial statements. Most startups will fall into this category. Read more for descriptions of projections and how to carry them out for your company.

The above methods are fast, efficient, and easy ways of determining the valuation of larger companies. Nonetheless, these methods will not work for early stage startups. This is for many reasons, mainly:

All of this goes to show that startups need their own special way of determining their value.

In order to better understand how to market yourself to potential investors, you also need to understand what they are looking for. To start off, investors are hoping for a 10-20x return on investment (ROI) 3-5 years after their initial investment. This is what they are hoping for, not necessarily what they always get!

Many investors typically don’t want to take more than a third (33%) ownership in your company. They don’t want to take too much because they want to leave the founders incentivized.

In terms of their ROIs, they expect that out of 10 investments, 4-5 are complete busts with $0 returns, 3-4 are a 1x return in 3-5 years (which is still a loss), and only 1 will be a “wow” with 10x or more ROI. You want to plan for your company to be a wow!

🔬Read: Understanding Pre-Seed and Seed Fundings For Startups

Now that you know what investors are looking for, you can learn the methods that many startups employ to value their business. Here is a list of a few popular methods:

Below we will dive a bit deeper into what each of these methods entails.

The Dave Berkus scorecard method uses both qualitative and quantitative factors to calculate valuation based on five different elements:

Each of these elements is then valued at a number between $0 and $500,000. Using this logic, the highest valuation would then have to be maxed out at $2.5 million. This method is good because it provides structure, and it reminds the investor of what they really care about (each of the five main elements).

Bill Payne was another investor that developed a slightly different scorecard method compared to Dave Berkus. Payne’s method involves similar categories, but each category can have a different weight. For example, see categories and their potential respective weights below:

| Factor | Weight | Rating | Comment |

|

Management |

30 | 125 | Full team |

|

Size of Oppt |

25 | 115 | Could be huge |

| Product/Service | 10 | 110 | Disruptive platform |

| Sales Channels | 10 | 70 | All foreign |

| Stage of Business | 10 | 125 | Prototype works |

| Other | 15 | 80 | Revenue non US |

Then, you would take a semi-arbitrary starting point and multiply your total result by that number. For the example above it would be $2,250,000 * 1.135 = $2,553,750. The $2,250,000 being the starting point. The starting point will differ based on region, product type, etc.

This method uses industry multiples, like the P/E ratio to determine a company’s value. You can use the method outlined earlier in this article to determine your own P/E ratio based on that of industry comparables.

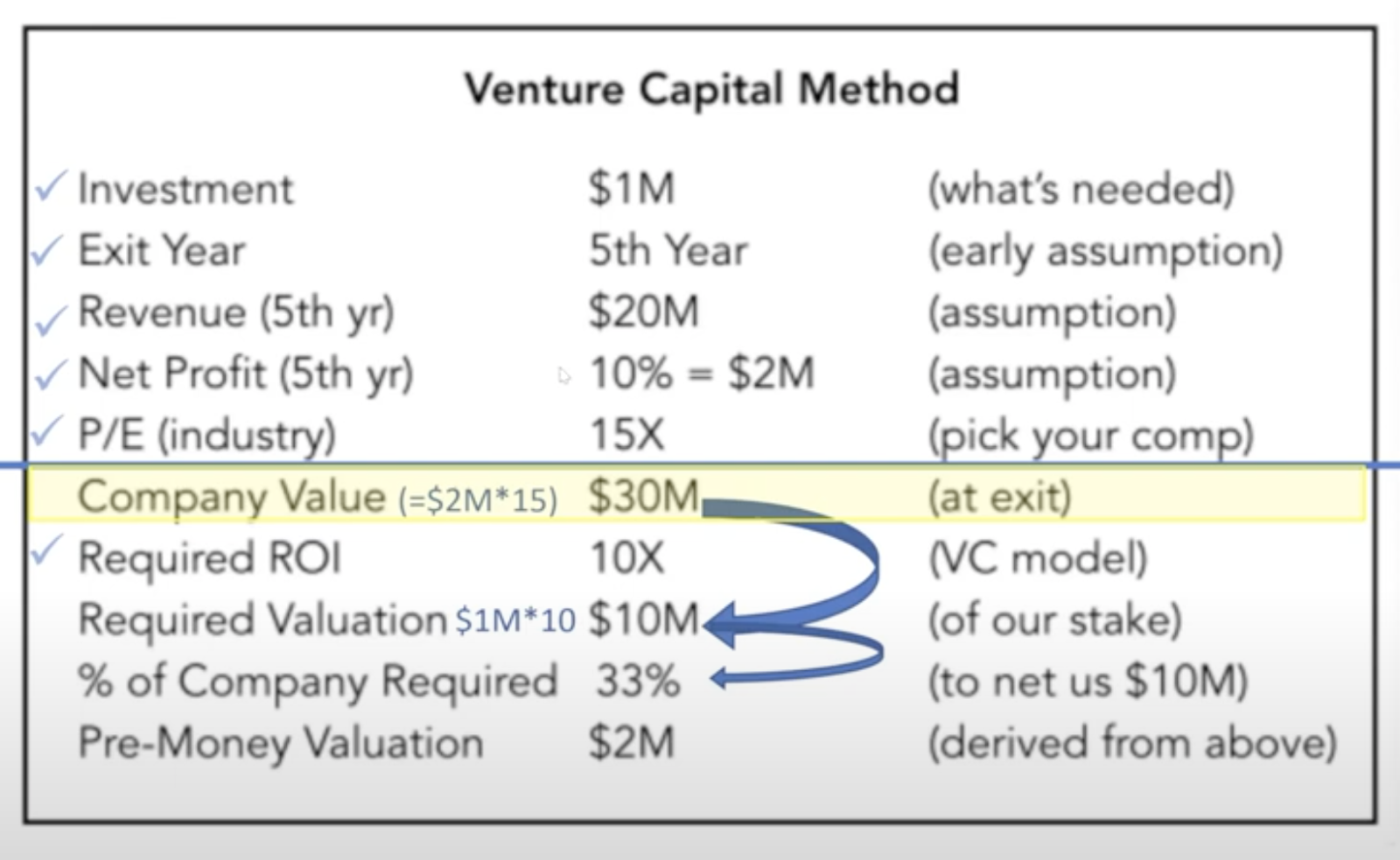

To complete this method, you will need to estimate your company’s future revenue, usually 5 years into the future. Then you use an estimated ROI and ownership percentage to calculate the investment needed to gain that particular ROI. See the graph below for more details:

The pre-money valuation is the current valuation of the company, $2 million in this case, and the $30 million is the valuation of the company at exit.

Here are the steps to complete:

State your assumptions: when you will exit and investor ROI expectations

Find your P/E ratio using the industry average

Gather your financial projections, like revenue and net earnings until exit

Calculate:

Value at exit: P/E * Earnings

Investor expectation at exit: ROI * Initial Investment

Investor expected share at exit: (Investor expectation at exit) / (Value at exit)

Then you will use all of this information to calculate the valuation pre and post investment: To do this, use the investor 's expected share percentage. For example: if the investor expects 33% ownership, and they initially invest $1 million, then the post-money valuation would be $3 million, and therefore the pre-money valuation would be $2 million.

However, this method can break down with some startups because it does not account for dilution and how that can change the investor’s ownership. It also can be ineffective for new startups that might not have revenue or profit in 3-5 years.

🔬Read: The Ins and Outs of Venture Capital Funding

Biotech startups are unique from other startups in three main ways:

Biotech companies have large failure rates that create only winners or losers, not many in between. This can cause investors to add a risk factor when assessing their investments. Long timelines are unappealing to investors, as they typically want a return in 3-5 years. However, biotech companies can take 12+ years to develop a drug, or even more for a Class III device. The high cash needs of early stage biotech companies signals to investors that they will mostly get diluted in the process. This could cause them to ask for higher shares in the company if they are investing early on.

Mergers and acquisitions (M&A) of biotech startups by larger corporations have become more popular in recent years. These activities de-risk the investment for each investor as they know there is a potential early exit.

The rising popularity of M&A in the industry can help biotech startups value their company by using the exit value for comparables that were acquired. Then you can predict how far in the future you will be acquired by a larger company based on your project timelines. Then use the time value of money equation to estimate the present value of your company.

Estimating your company’s value is an essential part of receiving funding. Investors want to know how you got the number you present to them, so be ready to have multiple explanations for them. The best approach is to try multiple different valuation methods, and see if they all produce a similar result. Then you can confidently say that your valuation is correct. It is also best to pick the most accurate value of your company, not just the highest. Choosing the fair value will prevent down-rounds and will be better for the company in the long run.

Q: How much equity should be given for how much investment?

A: The percentage will be determined based on the pre and post money valuation. You calculate the percentage using this formula: % Ownership = Investment / Post-Money Valuation

Q: How can you value a startup with multiple products that all stem from the same/similar technology?

A: This is a frequent situation for startups. The best choice is to look at multiple valuation methods, and try to find a comparable that has a similar business plan to your company.

This content comes from a webinar, Valuing Your Early Stage Biotech Company, featuring Dr. Molly Schmid in partnership with the SBDC @ UCI Beall Applied Innovation and University Lab Partners.

📽️ Watch the full webinar here.

Dr. Schmid brings more than 20 years of experience in the life science and small business technology industries and has held a variety of impressive leadership roles in bioinformatics, pharmaceuticals and health technologies, as well as the entrepreneurial space. She has also published several patents and publications. She was Vice President of Life and Health Technologies at ieCrowd, a global community of innovators where she coached Olfactor Laboratories, Inc. staff to transform novel vector control products into commercially viable technologies.

Be sure to subscribe to the ULP YouTube Channel to never miss another webinar, and connect with us on LinkedIn to stay in the loop!

Do you have a great company in the bioscience or medtech industry? Do you need wet-lab and/or fabrication space to develop and test your product?